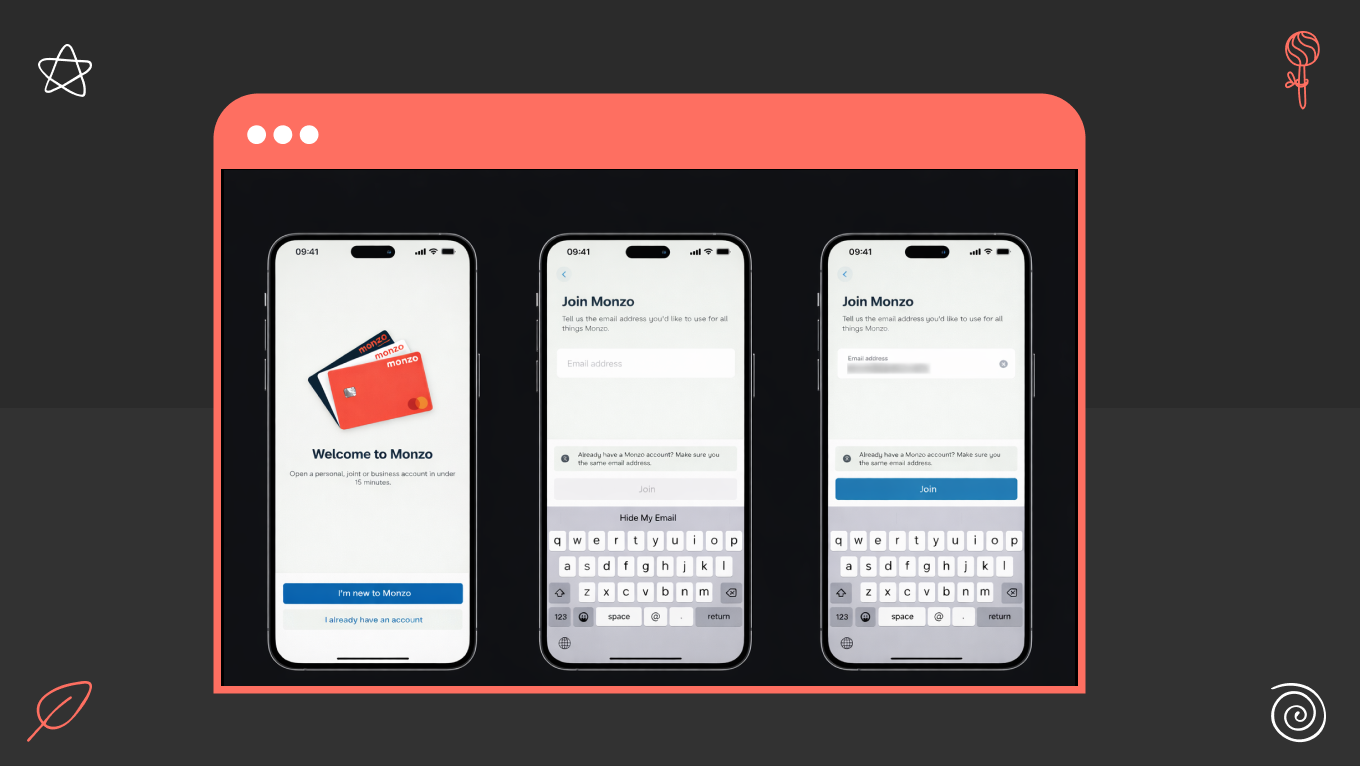

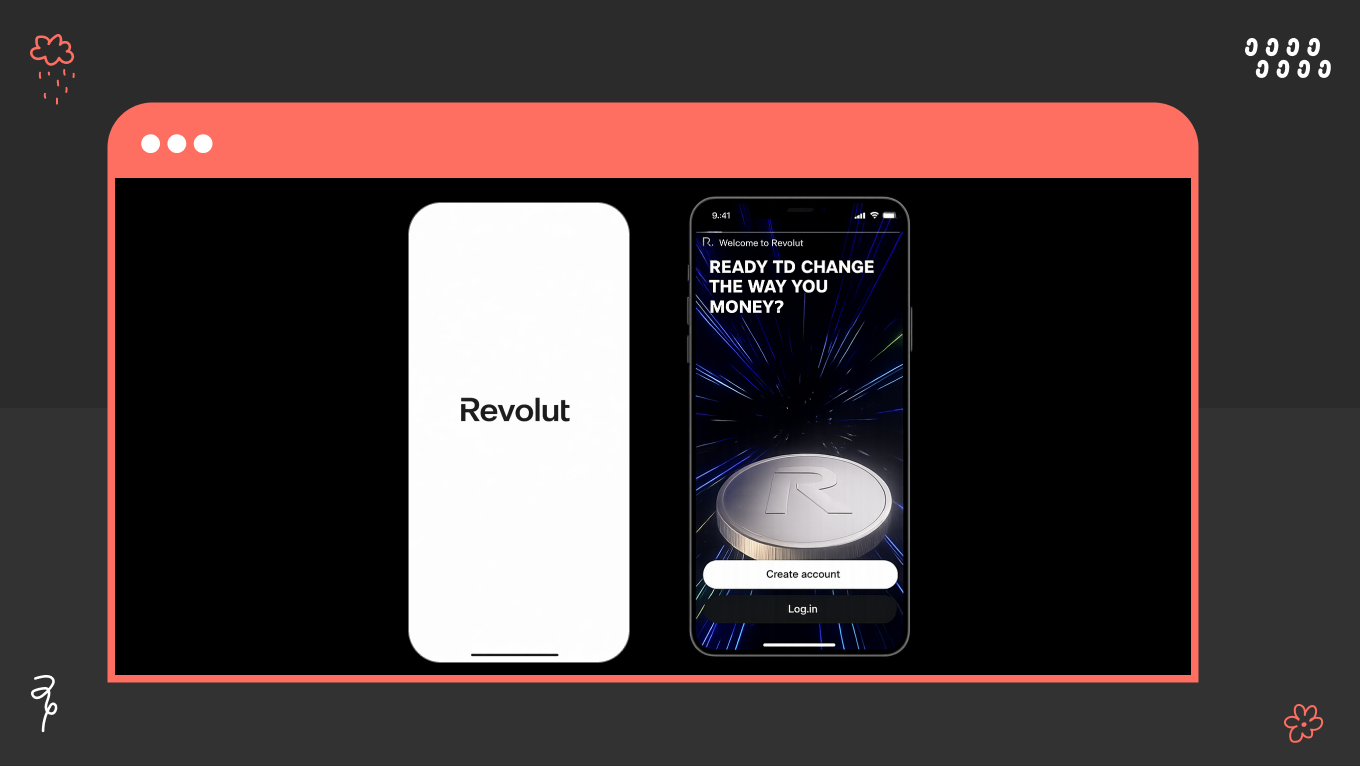

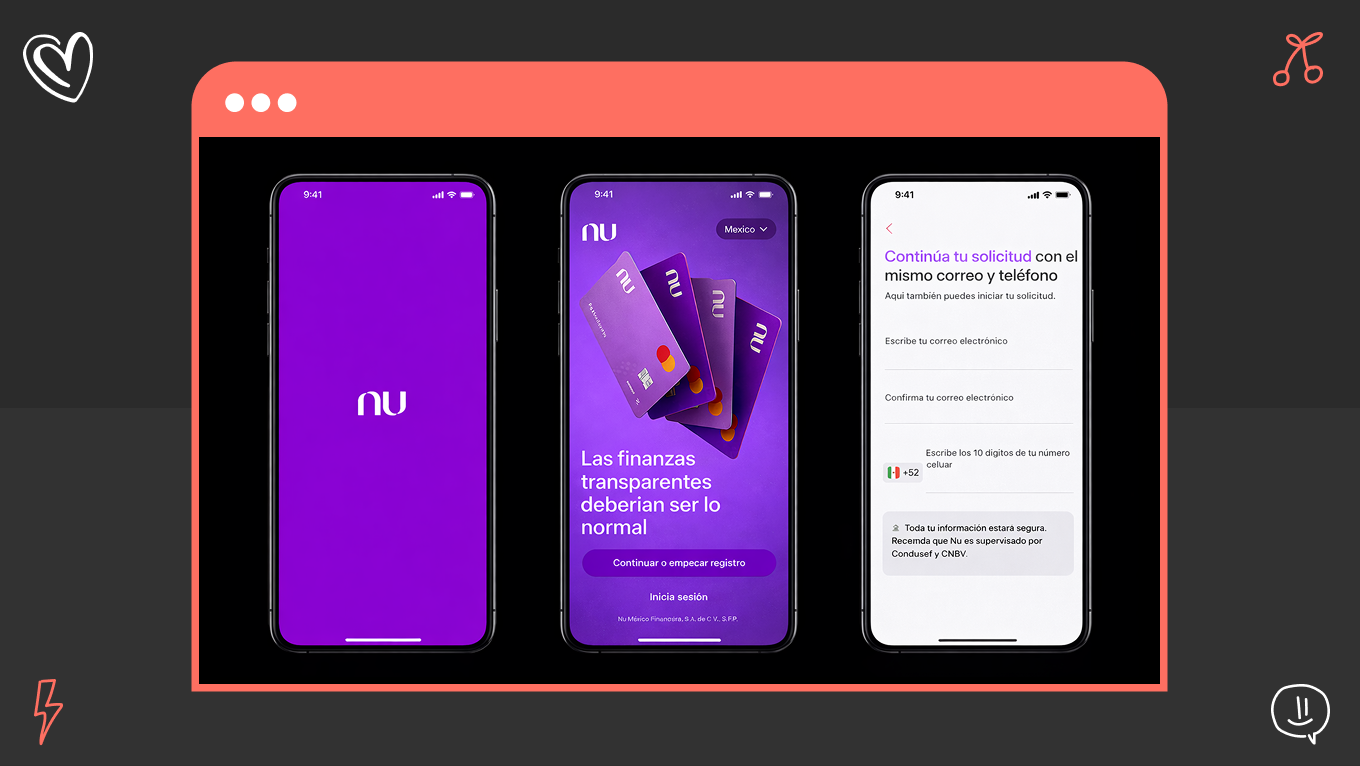

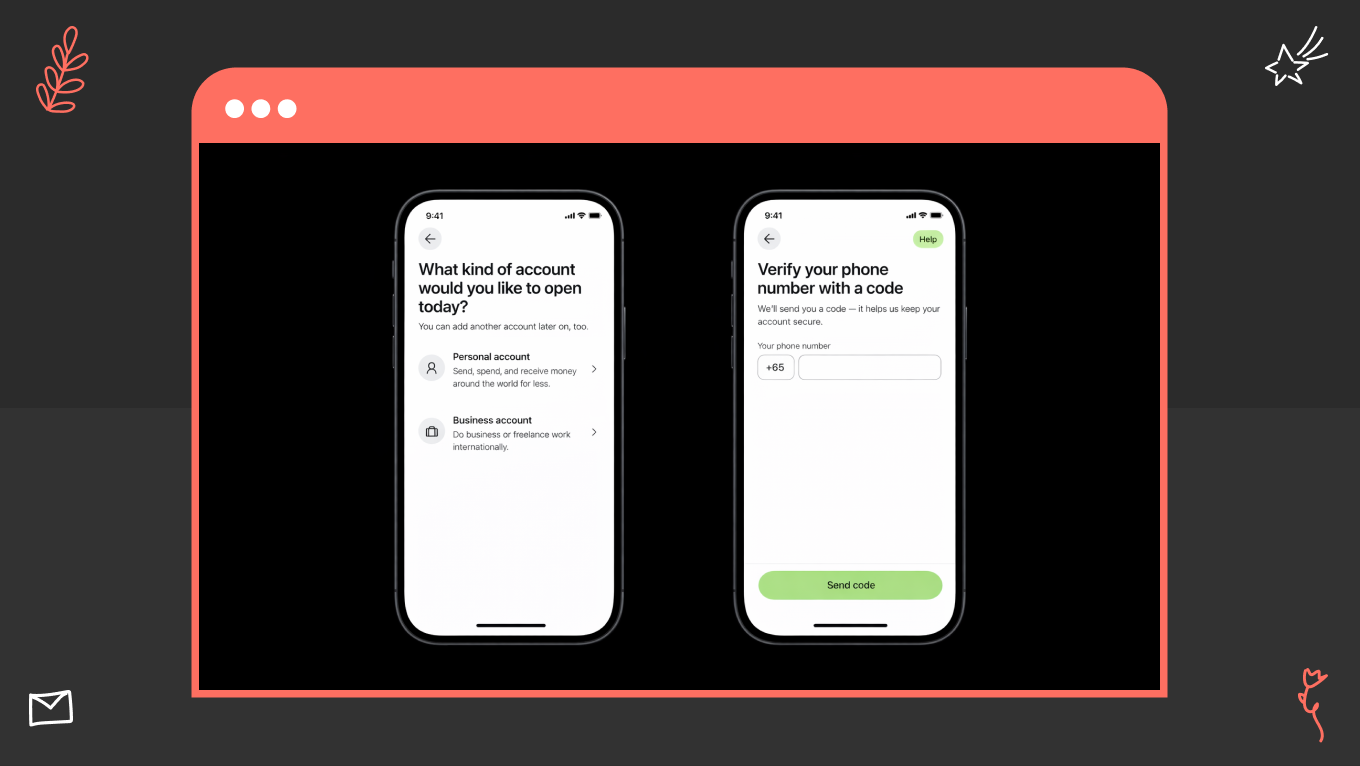

Your banking app design is one of the highest-leverage investments you can make in trust and retention. FCA reports that 75% of day-to-day account holders use mobile solutions, which makes them the main place customers experience your reliability. In practice, this means your UI and UX have to explain complex financial states with the same clarity every time, especially around payments, balances, cards, and verification.

A well-designed banking app goes beyond just improving the user interface. It serves as both a risk management tool and a driver of growth. When transaction states are clear, flows are predictable, and system behavior is easy to understand, customers can complete actions without needing support. They are comfortable moving larger amounts and return to the app more often, making it their primary financial channel.

With over 12 years of experience in mobile product design, Gapsy Studio created this guide for product owners and banking teams. We break down banking app design as an operating system. Also, our team covers UI, UX, service logic, and channel consistency. This way, you can make choices that reduce support needs, accelerate delivery, and improve customer retention.